Concerns the Russian invasion of Ukraine will draw more countries into the conflict raised risk and pushed global markets lower. Statements about nuclear forces going on alert and world leaders discussing a no-fly zone concerned investors.

Key Points for the Week

- Continued escalation from the Russian invasion of Ukraine is raising concerns about the risk of an expanded conflict.

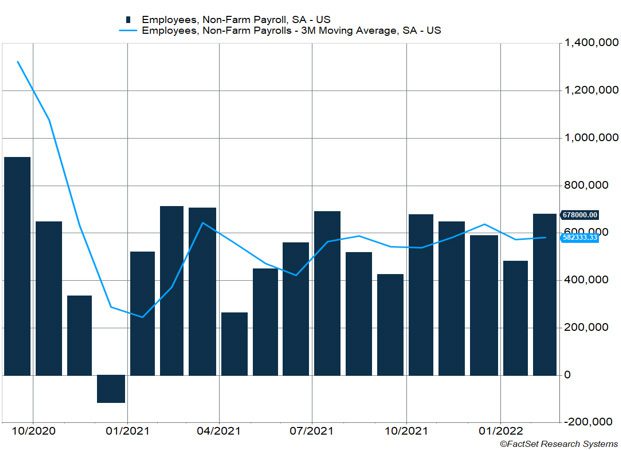

- U.S. establishment payrolls grew by an estimated 678,000 jobs last month. Unemployment slipped to 3.8% even as more workers returned to the labor force.

- Fed Chair Jerome Powell indicated he would recommend a 0.25% increase in interest rates at the Federal Reserve meeting next week.

Numerous countries and corporations have responded to the invasion by restricting the business they do in Russia or with Russian companies. Many retailers are no longer stocking Russian-made goods, and payment processing systems are stepping back from activity in Russia. Numerous sports leagues have cancelled matches in Russia as the world moves to punish the country for its attack on Ukraine.

The U.S. economy provided a bright spot for investors, creating 678,000 jobs, according to the establishment report. The household survey indicated unemployment dropped to 3.8% even though 300,000 people joined the labor force (Figure 1). Prior to the employment report, Fed Chair Jerome Powell stated he would recommend the Federal Reserve raise interest rates 0.25% at its meeting next week.

The S&P 500 slid 1.2% last week. The MSCI ACWI dropped 2.7% as international markets have been more affected by the increased risk created by the Russian invasion of Ukraine than U.S. markets. European stocks were a big reason for the decline. The MSCI Europe index dropped 9.6% last week. The Bloomberg U.S. Aggregate Bond Index rallied 0.9% as long-term rates fell sharply in response to the war potentially slowing economic growth and investors looking for more safety. We will continue to watch the ongoing conflict in Ukraine for market risk. The U.S. Consumer Price Index will provide an update on inflation this week.

Figure 1

Risk and Recovery

Normally the jobs report would have been very exciting for the market based on continued strength in the U.S. labor market. Instead, markets were dragged lower by the ongoing uncertainty in Ukraine.

Before commenting on Ukraine, let’s focus on the good news. The U.S. establishment survey estimated the economy added 678,000 jobs versus the expectation of a 400,000 gain, and the previous two months were revised higher by a combined 92,000 jobs. The U.S. added 1.15 million jobs in the first two months of the year, which is even more impressive considering the Omicron variant peaked in January. With these additions, the economy has regained about 90% of the jobs lost in March and April 2020, which is encouraging but shows many unfilled positions remain.

The household survey gave us more good news as the unemployment rate fell to 3.8%, down from 4% in January. What’s significant is that the unemployment rate fell while 300,000 more workers joined the labor force, meaning the economy was able to absorb them all. This puts the labor force only 300,000 participants below where it was pre-COVID-19 crisis. Average hourly earnings were flat last month, which may sound surprising given recent inflation trends. Looking deeper into the data, many of the jobs added were lower-paying positions in leisure and hospitality. That trend pushed the average down but doesn’t signify wage pressures are lessening.

So, the economy added a lot of jobs, the labor market grew, and it’s been more successful in filling the hard-to-fill jobs. What does this mean for the Fed? This is almost certainly giving the Fed the all-clear to raise rates this month. Based on Powell’s testimony to Congress last week, the Fed has signaled its intention to raise rates 0.25% at this meeting and then see how quickly rates must rise to curb inflation.

Charting the right path on interest rates will be challenging, but not nearly as much as analyzing the risks from Ukraine. Last week we introduced a three-part framework for evaluating how markets would likely be affected.

- Adverse economic consequences of sanctions

- Risks of escalation

- Long-term consequences

Each part of the framework experienced some important shifts last week. The consequences of sanctions are increasing. U.S. Secretary of State Antony Blinken announced the U.S. and its allies are considering banning Russian oil and gas imports to further pressure Russia economically. In response, oil prices have shot higher and gasoline prices will likely follow. Replacing Russia’s production will be difficult and take time, pushing oil prices higher and threatening Europe’s economy. Other commodities have also increased in price.

Many global corporations have implemented sanctions of their own. Payment processors are stepping back from the Russian market. Firms are choosing not to supply parts to existing customers, and technology companies are also cutting ties. Retailers are responding by removing Russian products from their shelves.

Russian President Vladimir Putin’s order to place the country’s nuclear forces on higher alert and talk of a no-fly zone enforced by NATO contributed to an increased risk of escalation. The degree of sanctions and the large number of corporate entities that have withdrawn from Russia are expected to force the Russian economy into a massive decline. How Russia responds to the sanctions carries its own risks. The 9.6% decline in the MSCI Europe Index reflects concerns about how sanctions will affect Europe as well as the risk of escalation.

The long-term consequences of the attack seem to point to a more dangerous world and the possibility of a protracted conflict. One immediate consequence is Russian stocks will be removed from the three major global indexes this week, a shift that is unlikely to be reversed anytime soon. This means most investors will have no exposure to Russian stocks by the end of this week.

In uncertain times it is key to keep perspective while being realistic that risks have increased. Sometimes investors focus on getting the risk level right for their overall portfolio, which can be very effective. Another method is to think about how soon you might need money from your portfolio. Having adequate short-term investments set aside for withdrawals may give you confidence about the short term while allowing the higher-risk portions of your portfolio time to recover if the decline worsens. If you have questions during uncertain times, please reach out to your advisor.

–

This newsletter was written and produced by CWM, LLC. Content in this material is for general information only and not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be invested into directly. The views stated in this letter are not necessarily the opinion of any other named entity and should not be construed directly or indirectly as an offer to buy or sell any securities mentioned herein. Due to volatility within the markets mentioned, opinions are subject to change without notice. Information is based on sources believed to be reliable; however, their accuracy or completeness cannot be guaranteed. Past performance does not guarantee future results.

S&P 500 INDEX

The Standard & Poor’s 500 Index is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

MSCI ACWI INDEX

The MSCI ACWI captures large- and mid-cap representation across 23 developed markets (DM) and 23 emerging markets (EM) countries*. With 2,480 constituents, the index covers approximately 85% of the global investable equity opportunity set.

Bloomberg U.S. Aggregate Bond Index

The Bloomberg U.S. Aggregate Bond Index is an index of the U.S. investment-grade fixed-rate bond market, including both government and corporate bonds.

MSCI Europe Index

The MSCI Europe Index captures large and mid cap representation across 15 Developed Markets (DM) countries in Europe*. With 429 constituents, the index covers approximately 85% of the free float-adjusted market capitalization across the European Developed Markets equity universe.

https://www.bls.gov/news.release/empsit.nr0.htm

https://www.wsj.com/articles/what-putins-nuclear-threats-mean-for-the-u-s-11646329125

https://www.cnbc.com/2022/03/06/stock-market-futures-open-to-close-news.html

Compliance Case # 01296122